It’s not a million dollars. It’s not six figures. The real wealth-building milestone is smaller than you think — and far more powerful.

That Feeling When You Actually Smile at Your Bank Account

You know that feeling when you check your bank account and instead of immediately closing the app in horror, you actually smile? When you stop calculating whether you can afford that coffee, or whether buying groceries means eating ramen for the rest of the week?

There’s a specific number where this shift happens — and it’s not what most people think. Most financial gurus will tell you that you need a million dollars to feel wealthy, or that six figures is the magic number. But here’s what they’re missing: there’s a much smaller milestone that completely transforms your relationship with money. And once you hit it, everything changes.

That number is $20,000.The $20000 savings rule is the most underrated milestone in personal finance.

Before we dive in, let me ask you something. When you think about building wealth, what comes to mind? Maybe you picture some trust fund kid who never had to worry about money. Or perhaps you imagine someone grinding away for years, slowly accumulating wealth $1 at a time. The truth is, wealth building doesn’t work the way most people think it does.

The Invisible Barrier Most People Never Cross

The $20000 savings rule proves that you don’t need millions to change your financial life.There are certain financial thresholds that act like invisible barriers. Once you cross them, the rules of the game completely change. $20,000 is the first major threshold that separates those who will build significant wealth from those who will spend their entire lives living paycheck to paycheck. And the crazy part? Most people have no idea this threshold even exists.

Think about it this way. If you’ve ever tried to push a heavy boulder up a hill, you know that getting it started is the hardest part. You’re straining, sweating, making very little progress, and questioning whether it’s even possible. But once you build enough momentum, something magical happens — the boulder starts moving faster, and eventually when you reach the top, it rolls down the other side almost effortlessly.

$20,000 is that turning point. Everything before this feels like you’re pushing uphill against gravity. Everything after feels like gravity is finally working in your favor.

The Brain Science Behind the Number

The difference isn’t just mathematical. It’s not simply that you have more money to invest. The real magic happens in your brain.

When you don’t have money saved, your brain operates in what psychologists call survival mode. Every financial decision is filtered through fear and scarcity. You take the first job offer that comes along, even if it’s terrible, because you can’t afford to be picky. You stay in situations you hate because leaving feels too risky. You say yes to things you don’t want to do because you need the money.

This isn’t just about being practical. When you’re in survival mode, your brain literally cannot think about growth and opportunity. It’s like trying to plan a vacation while your house is on fire. Your mental bandwidth is completely consumed by immediate threats.

But something remarkable happens when you apply the $20000 savings rule and cross that threshold. Instead of asking ‘How do I survive until next paycheck?’ you start asking ‘How can I grow this money?’ Instead of being reactive to every financial crisis, you become proactive about building wealth.

Research from Vanguard shows that having just $2,000 in emergency savings increases financial well-being by 21%. Push that to 3–6 months of expenses (around $20,000 for most people) and you get another 13% boost — plus the mental shift that changes everything

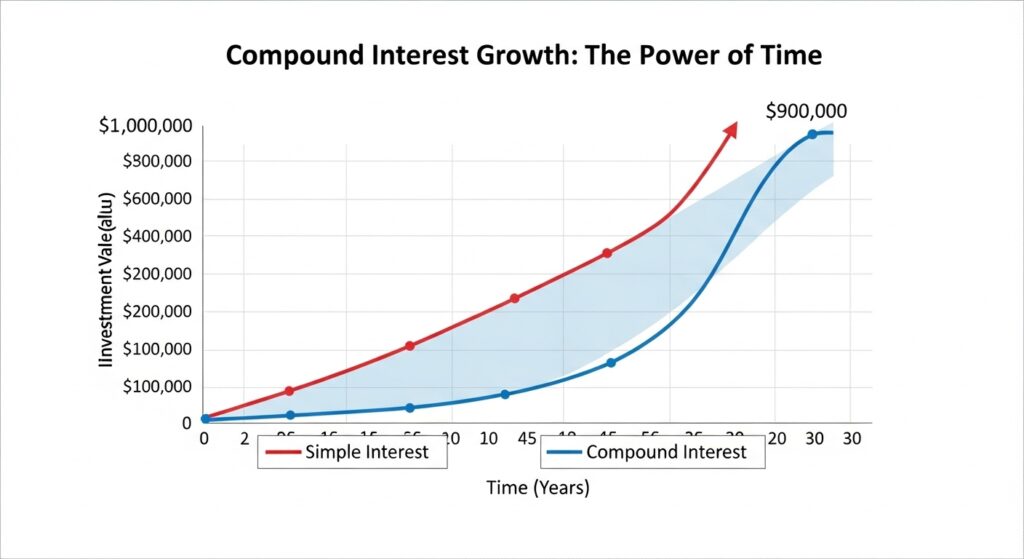

The Math That Will Blow Your Mind: Compound Interest in Action

Let’s say you’re saving $1,000 every month and earning an 8% annual return on your investments.This is exactly why the $20000 savings rule works — the math is on your side. Getting to your first $20,000 takes about 19 months of consistent saving and investing. That’s a year and a half of discipline, sacrifice, and delayed gratification. It’s not easy — and frankly, most people give up somewhere along the way.

But here’s the part that changes everything: your second $20,000 doesn’t take another 19 months. It only takes about 17 months. Why? Because now you’ve got that first $20,000 working alongside your monthly contributions, generating its own returns.

You did the exact same amount of work. Saved the same amount each month. Took the same level of risk. But you shaved two full months off the timeline just because you had more money working for you. That’s the power of compound interest starting to kick in.

When Your Money Does the Heavy Lifting

By the time you’re going for your third $20,000, the timeline shrinks even more. And when you get to the really big numbers, the acceleration becomes almost unbelievable.

Once you hit $400,000 in your investment portfolio, you can generate your next $20,000 in just 5 months — automatically, through your investments alone.

The same amount that took you nearly two years to save initially is now happening on autopilot. That first milestone feels impossible, but every milestone after that gets progressively easier. This isn’t magic — it’s basic mathematics finally working in your favor.

A 10% return on $2,000 is $200. A 10% return on $20,000 is $2,000. Same strategy, same time frame, same level of risk. The only difference is scale — and that scale transforms small percentage wins into real financial progress.

The Hidden Superpower of Saving $20,000: What It Does to Your Brain

When you follow the $20000 savings rule and hit that milestone, you’ve accomplished something far more valuable than just accumulating money in a bank account. You’ve fundamentally rewired your brain and built the most important financial habit you’ll ever develop.Think about what it actually takes to save $20,000 starting from zero. Unless you’re making serious money or have zero expenses, this requires real discipline. You had to track where every dollar was going. You had to say no to things you wanted so you could set money aside instead. You had to resist the urge to blow your savings on whatever shiny object caught your attention that week. And most importantly, you had to do all of this consistently for months — or even years.

You proved to yourself that you can control your money instead of letting it control you. That’s not just a financial skill. That’s a life skill.

Small Expenses Stop Stressing You Out

Before you had $20,000 saved, buying a $4 coffee might have required mental gymnastics about whether you could afford it. After you hit $20,000, you’re not sweating the small stuff anymore — because you know you have your priorities straight and you’ve proven you can make the big sacrifices when they matter.

Here’s something counterintuitive that most people miss: once you build a solid financial foundation, you actually start caring less about small expenses and more about the big ones.

The difference between spending $5 on coffee versus making it at home is maybe $1,000 per year if you’re going overboard. That’s not nothing, but it’s not going to make or break your financial future. What matters are the big decisions: where you live, what you drive, how much you save, where you invest. These choices can swing your net worth by tens of thousands of dollars over time.

This shift in focus is incredibly liberating. You stop sweating the small stuff and start thinking strategically about wealth building.

How $20,000 Transforms Your Career and Negotiating Power

Having $20,000 saved doesn’t just change your relationship with money. It changes your relationship with work.

When you’re living paycheck to paycheck, you’re essentially trapped in whatever job you currently have. Your boss could be terrible. Your coworkers could be toxic. The work could be mind-numbing. But you can’t leave because you need that next paycheck to survive. This puts you in an incredibly weak negotiating position. You can’t ask for a raise because you’re afraid they might fire you. You can’t push back on unreasonable demands because you need the job more than they need you.

Your ‘Walking Away Money’ Changes Everything

The $20000 savings rule gives you what I call walking away money — and it changes everything at work. You could quit tomorrow and survive for months while you find something better. This doesn’t mean you should be reckless or burn bridges unnecessarily — but it means you’re negotiating from a position of strength instead of desperation.

You start asking for the raise you deserve because the worst they can say is no, and you’ll be fine either way. You push back on unreasonable requests because you’re not afraid of the consequences. You explore new opportunities because you can afford to take some risk.

Here’s what’s really interesting: often you don’t even need to use your walking away money. Just having it changes your entire demeanor at work. You become more confident, more assertive, more willing to take on challenging projects. And guess what happens when you show up differently? People notice. You start getting better assignments, more recognition — and yes, more money. It’s a positive feedback loop that accelerates over time.

The Biggest Mistake People Make After Hitting $20,000

Here’s where most people mess this up — and it’s more common than you’d think.

They hit $20,000, feel that psychological shift, and then immediately blow it on something stupid. Maybe they decide they deserve a new car since they’ve been so disciplined. Or they take an expensive vacation because they’ve ‘earned it.’ Or they use it as a down payment on a house they can’t really afford.

Don’t do this. That $20,000 is not a reward for good behavior. It’s the foundation of your entire financial future.

The Car Trap: America’s Most Expensive Habit

The average American spends more money on their car over their lifetime than it would take to achieve complete financial independence. Between car payments, insurance, maintenance, and gas, most people are spending $600 to $800 every single month on transportation. Over a 40-year period, that’s easily $400,000 or more just to get from point A to point B.

And here’s the part that makes it even worse: the moment you drive a new car off the lot, it loses about 20% of its value. You’re not just spending money — you’re actively destroying wealth.

Compare that to investing the same amount in a diversified portfolio. That $30,000 car isn’t just $30,000. It’s $30,000 that could have grown to over $200,000 in your investment account over 20 years.

Suddenly, driving a reliable used car doesn’t feel like a sacrifice. It feels like a strategic choice that’s funding your future freedom. And here’s the beautiful irony: the person driving the flashy new car is probably stressed about money, while the person driving the older Honda is quietly building wealth — and sleeping better at night.

You Start Seeing Opportunities You Never Noticed Before

When you’re living paycheck to paycheck, every unexpected expense feels like a disaster. Your car needs repairs — financial emergency. Your laptop dies — crisis. Your rent goes up — catastrophe.

But when you have $20,000 in the bank, these same events become minor inconveniences at worst. Your car needs repairs? Annoying, but not catastrophic. Your laptop dies? Time to upgrade to something better. Your rent goes up? Maybe it’s time to negotiate your salary or find a better place.

Even better, you start noticing opportunities that were always there, but you couldn’t take advantage of before. Your friend mentions they’re starting a business and looking for investors. Before, you would have thought ‘that sounds interesting’ and moved on. Now you can actually consider whether it’s worth putting $5,000 into it. A great deal pops up on a rental property. Before, you’d scroll past it feeling envious. Now you can run the numbers.

This is what wealthy people mean when they say ‘money goes to money.’ It’s not a cosmic conspiracy. It’s that having money gives you options — and options create more opportunities to make money.

Start Building That Foundation Today

$20,000 isn’t going to make you rich overnight. But it will fundamentally change how you think about money and opportunity. It’s the difference between surviving and thriving — between reacting to life and designing it.

Once you start thinking in terms of opportunity cost, you often realize you don’t actually want half the stuff you thought you wanted. That bigger apartment? The extra space would be nice, but is it worth delaying your financial independence by 5 years? That expensive hobby? There are probably cheaper ways to get the same satisfaction.

This isn’t about becoming a penny-pinching miser who never enjoys anything. It’s about becoming intentional with your money — making choices that align with what you actually want your life to look like.

Remember the $20000 savings rule — it’s not just a number, it’s the foundation of your entire financial future. Start today. Set up an automatic transfer to your savings or investment account. Make it non-negotiable. Your future self is counting on the decisions you make right now — and trust me, they’ll thank you for it.

Enjoyed this post? Share it with someone who needs to hear it. And drop a comment below — what’s your biggest challenge in hitting that $20,000 milestone?

— Inspired by Haseeb financial psychology insights